Service Consistency is Harder, and Rarer, Than Service Quality

Any financial institution can deliver a great moment. The best financial institutions can repeat those great moments consistently.

Most financial institutions are good at the highlight reel moments that get customers in the door. A loan officer who stays late to close a mortgage for a new customer. The 6% APY teaser rate campaign on checking accounts caused a surge of new accounts. Those moments and interactions are real, and they matter.

But those moments aren’t how to improve customer service in banks and credit unions, and they aren’t what create loyal customers. In fact, things like value banking are actually what make for disloyal customers, with one study showing that one-quarter of consumers would switch or have already switched financial institutions becuase a bank or credit union offered a cashback/rewards program.

What gets the consumer in the door isn’t what makes them a loyal customer or member. Even a moment of great customer service won’t do it. So what does? Consistency.

The Consistency Game Changer

A customer's opinion isn't formed by their best interaction with an institution. It's formed in the gap between their best and their worst. The customer who has a warm branch visit on Monday and then hits a dead end in a mobile app on Tuesday doesn't average those into “pretty good.” They remember the friction. And increasingly, they have somewhere else to take their daily banking.

That’s the challenge for financial institutions right now, especially community banks and credit unions. How do institutions keep customers and members when they can probably find another bank with higher rates or lower fees?

That’s where consistency comes in. A great first impression might not prevent a customer from leaving for greener grass at another financial institution, but consistently positive interactions might. Consider these two statistics.

First, according to Raisin’s 2026 Consumer Banking Trends report, over 50% of respondents to a recent study said customer service motivated whether or not they stay or leave. So yes, customer service in banking can drive loyalty, even when faced with competitors that offer superior products or digital features.

However, according to Capgemini's World Retail Banking Report, only about 25% of customers say they're satisfied with their core banking experiences, and they are no longer comparing their bank to other banks. They are comparing it to the seamless, instant experiences they get from the best digital brands they use every day. Against that standard, an institution that is excellent in the branch or on the phone, but clumsy online, isn't delivering good service. It is delivering inconsistent service, which reads as unreliable.

How To Improve Customer Service in Banks and Credit Unions With Consistency

This is where consistency gets genuinely hard. Quality within a single channel is largely a function of hiring good people and training them well. Consistency is structural. The branch, the call center, the app, and the website all have to know the same things about the member and behave in compatible ways. When a customer explains their situation to a branch employee and then has to repeat the whole story to a call center agent an hour later, the institution has just told them their time doesn't matter, no matter how friendly both employees were.

J.D. Power's retail banking research has found that frontline roles, including tellers, service reps, and call center agents, often draw some of the lowest satisfaction scores, particularly from younger customers. This is counterintuitive to what we know and understand about customer service in banking. It isn’t that the personal interactions financial institutions have with customers are all terrible, but that they don’t consistently resolve problems. This unresolved friction is a leading driver of “silent attrition,” where a customer quietly opens a secondary account elsewhere rather than leaving outright.

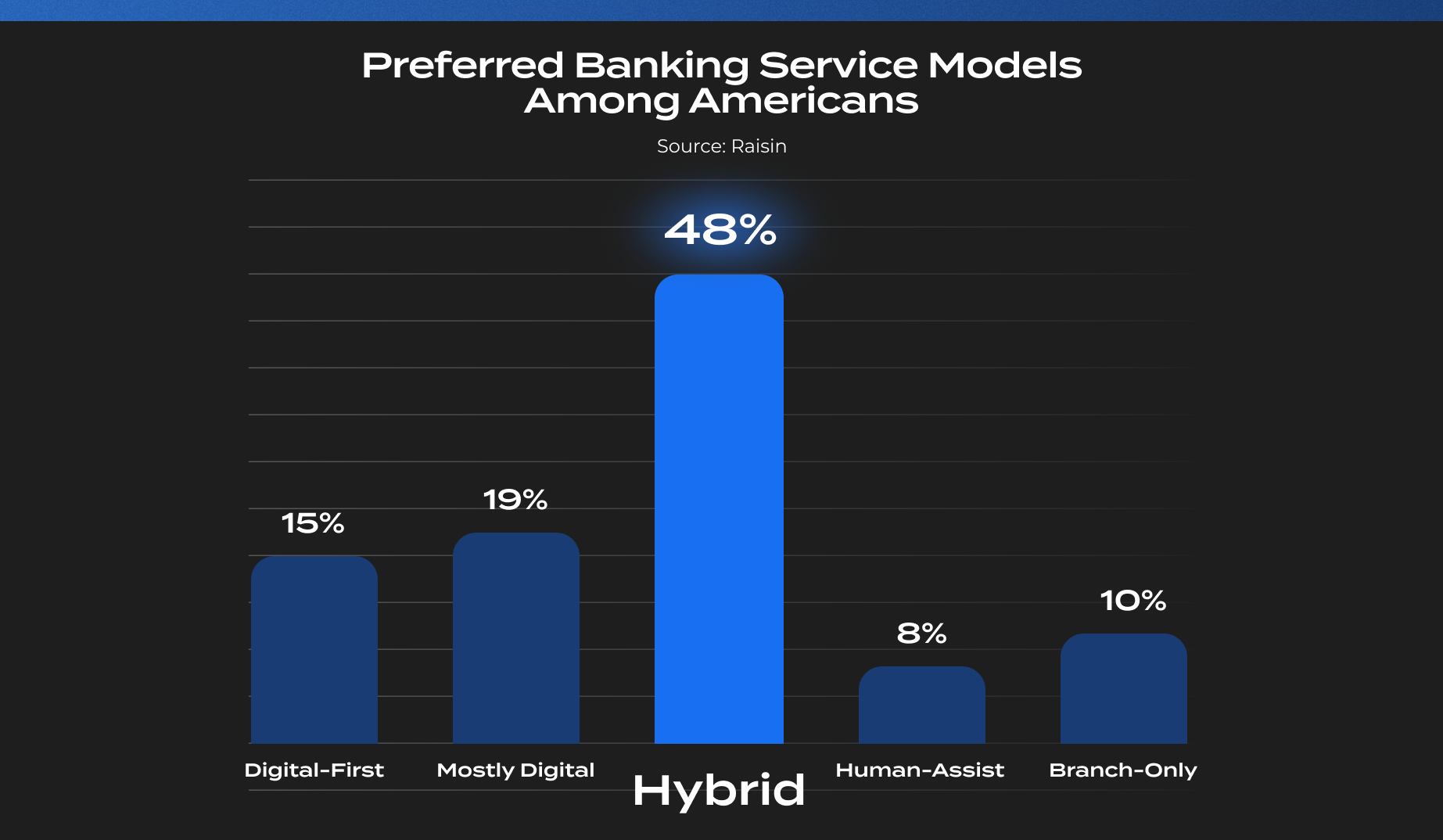

To fix this, we have to stop viewing customer service at the surface level and start viewing it as a comprehensive effort. Even in 2026, most people still prefer both digital and physical options. Community banks and credit unions simply cannot afford to trade one for the other, because that is the sort of inconsistency that leads to turnover.

If customers can’t get the exact same level of attention and service from the channel they want, they’ll look for a financial institution that can provide it for them.

Consistency Starts One Interaction At A Time

The fix is rarely a single heroic effort. It is the unglamorous work of closing gaps: making sure a question answered in one channel doesn't have to be re-asked in another, keeping wait times predictable rather than wildly variable, and making sure the experience doesn't fall apart the moment a member steps outside the branch.

Service quality wins you a compliment. Service consistency wins you the relationship. For community institutions whose whole pitch is “we treat you better,” consistency isn't a nice-to-have. It is the proof.